Cindy Ord/Getty Images Entertainment

Robinhood Markets, Inc. (NASDAQ:HOOD) has finally broken out, it seems. After trading in the $10 range for nearly 2 years, HOOD has finally returned to $20, though it has since pulled back from that recent high. What was the catalyst? It appears that investors are optimistic about the company’s newly announced Robinhood Gold Card, which offers 3% cash back on everything and may help accelerate asset growth. The company is GAAP profitable and maintains a very strong net cash balance sheet. The stock is no longer as cheap as it was just several months ago, but improving sentiment and the possibility of accelerated growth may help justify further upside. I reiterate my buy rating for the stock.

HOOD Stock Price

I last covered HOOD in December, where I highlighted the potential catalyst in the X1 credit acquisition. The company has since unveiled the highly anticipated card offering, and the stock is up 30% since then.

Despite the stock run-up, I continue to see value ahead as the stock has more run to room if the company can return to being a high-growth story.

HOOD Stock Key Metrics

HOOD is a stockbrokerage firm most well known for pioneering the commission free trading model. The brokerage industry is largely viewed as being commoditized, and for good reason, but HOOD has attempted to continue rolling out product “innovations” (put in quotes because many of their features can arguably be easily replicable by competitors).

2023 Q4 Presentation

With HOOD, the advantage is not necessarily in having some unique feature, which it does not appear to have. Instead, HOOD appears to be attacking an opportunity made possible due to legacy brokerage firms focusing more on fees and less on consumer satisfaction (at least in my humble opinion). HOOD has directly taken on larger incumbents through its easy-to-use UI, but most importantly, its generous perks.

2023 Q4 Presentation

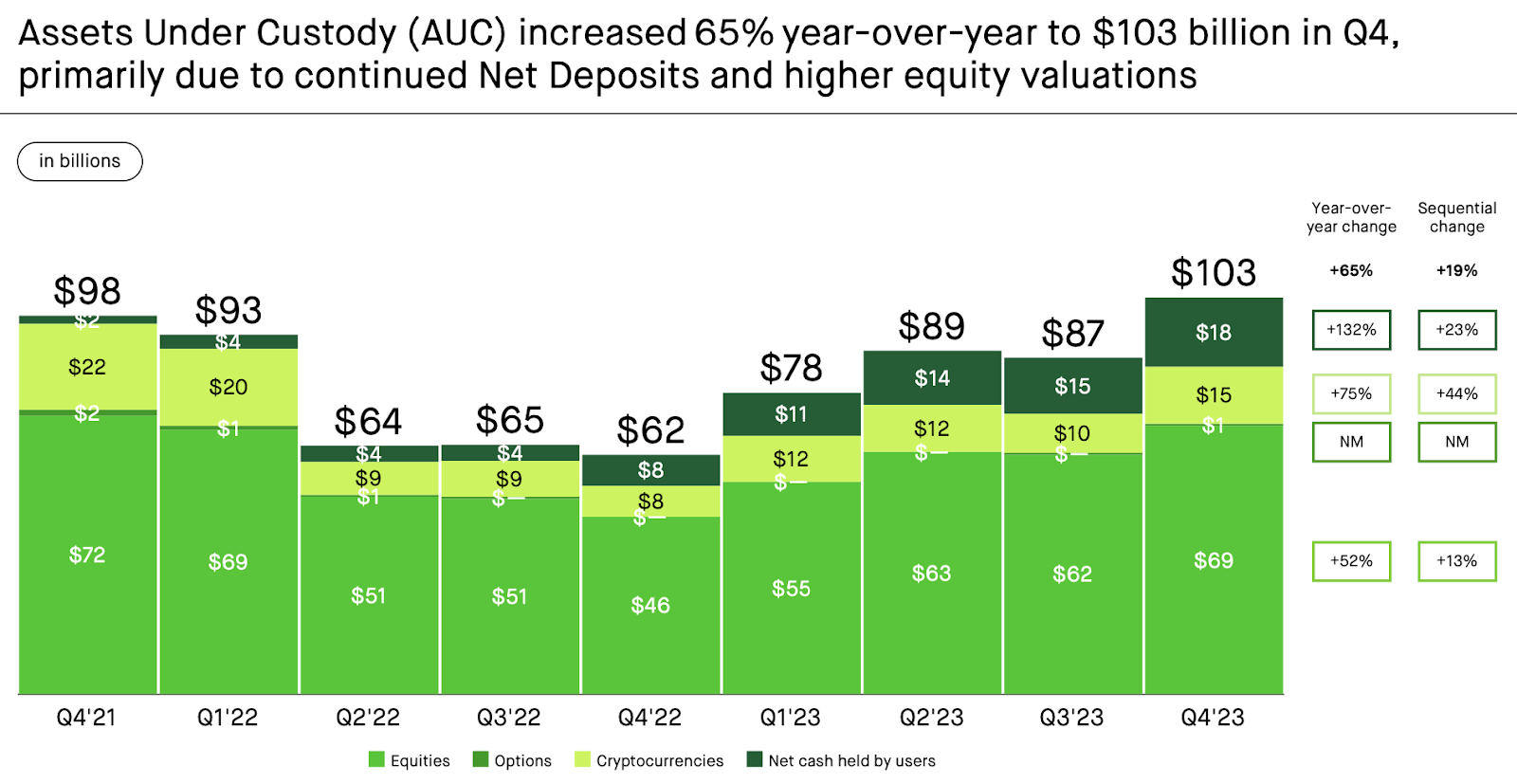

In the latest quarter, HOOD saw assets under custody grow 65% YoY with a broader market rally fueling much of the gains. Given the strong start to equities this year, I expect this upcoming quarter to see more of the same (next release expected post-market May 8th).

2023 Q4 Presentation

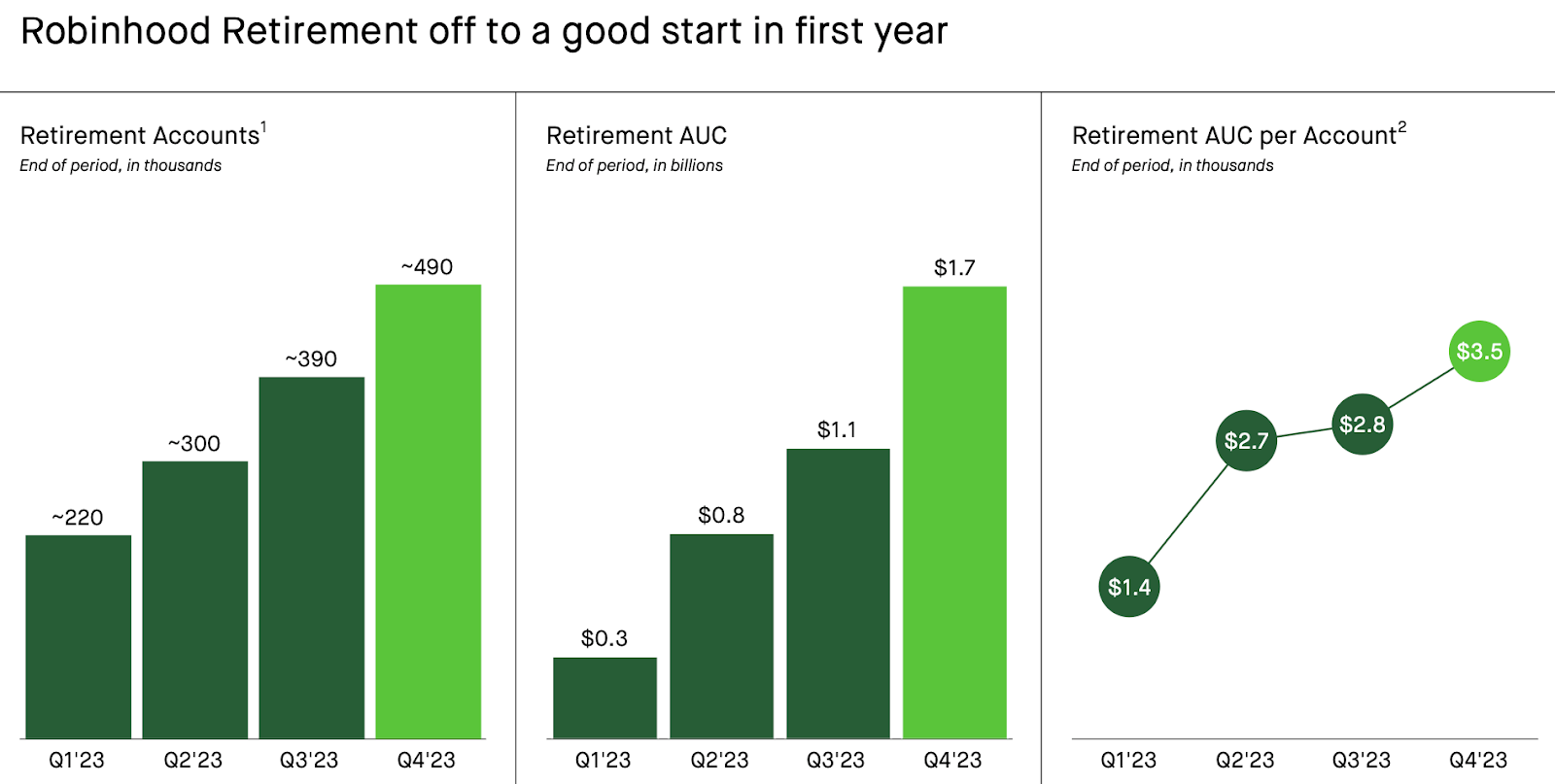

HOOD unveiled retirement accounts to the public in January of last year and has seen incredible growth. It helps that HOOD offers a 1% match on IRA contributions.

2023 Q4 Presentation

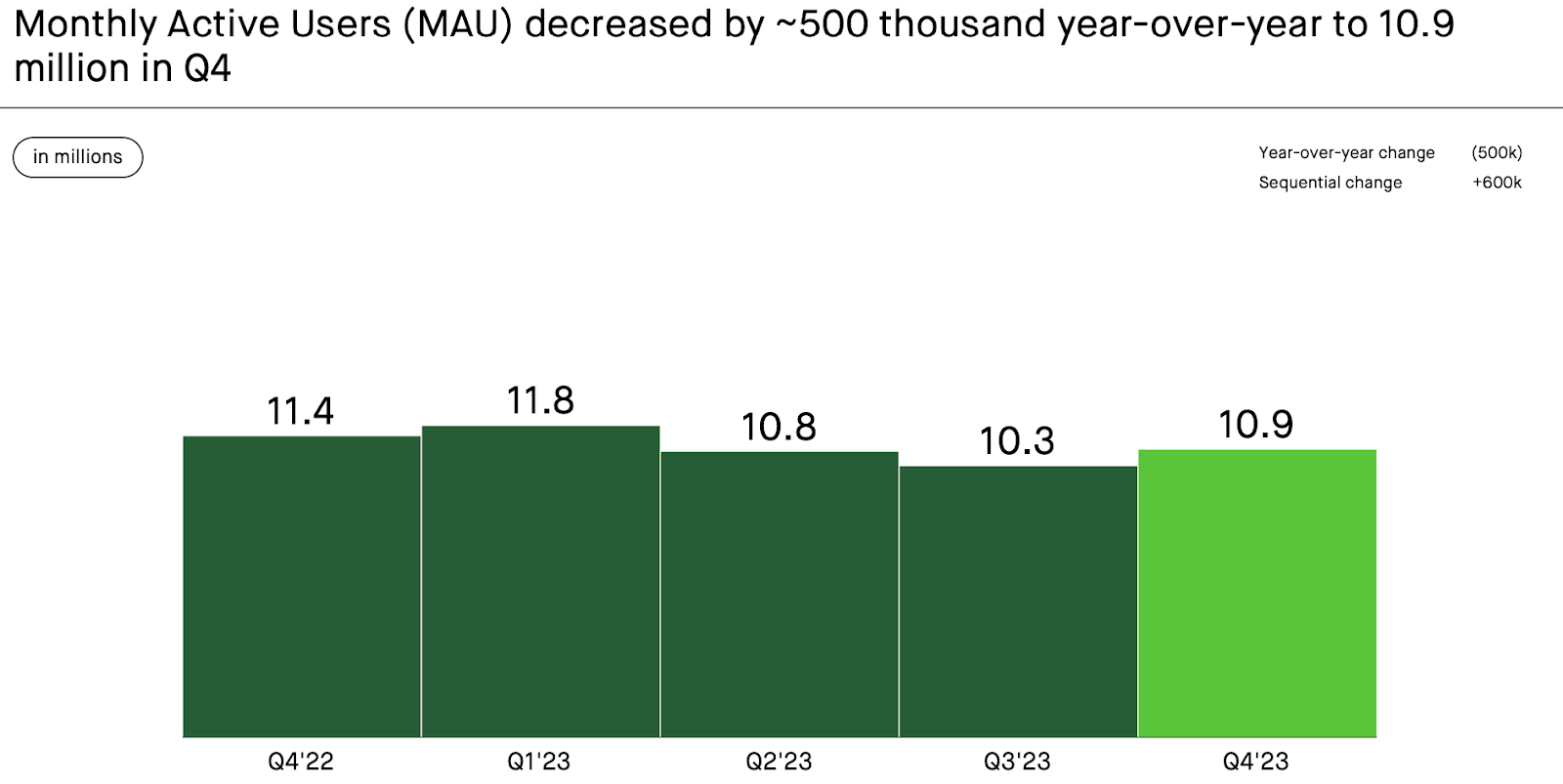

HOOD saw some stabilization in monthly active users (“MAU”) as MAUs grew 5.8% QoQ, but still fell by 4.4% YoY.

2023 Q4 Presentation

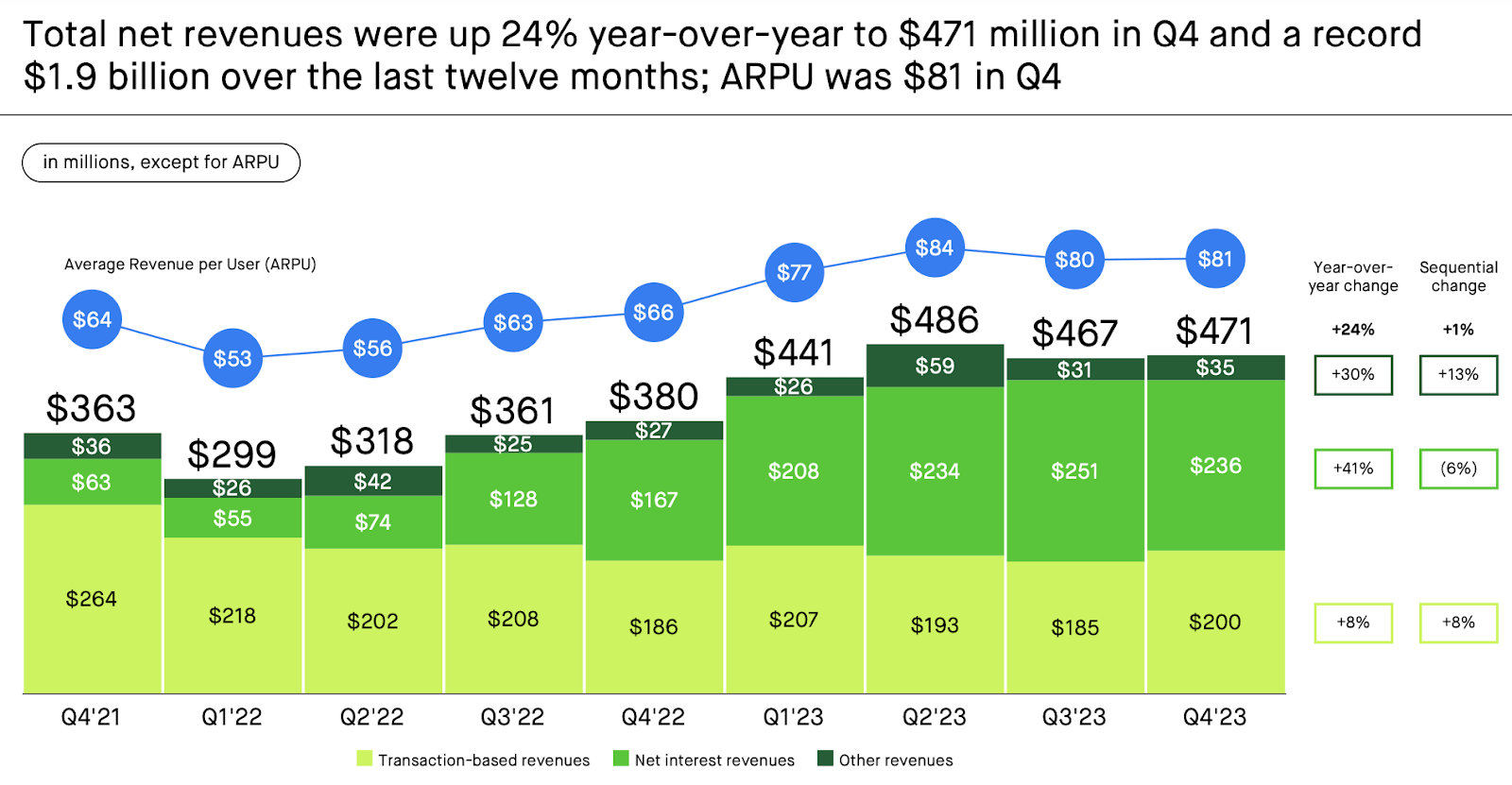

The company saw net revenues grow by 24% YoY, boosted by 41% YoY growth in net interest revenues as the company benefited from the higher interest rate environment.

2023 Q4 Presentation

Some readers may notice that this past fourth quarter represents a full-year of higher interest rates. That means that the company is unlikely to see similar YoY growth rates in net interest revenues, as these strong results become tough comparables. On the flip side, the company saw transaction-based revenues grow 8% YoY in the quarter, the only quarter in 2023 which did not see YoY declines.

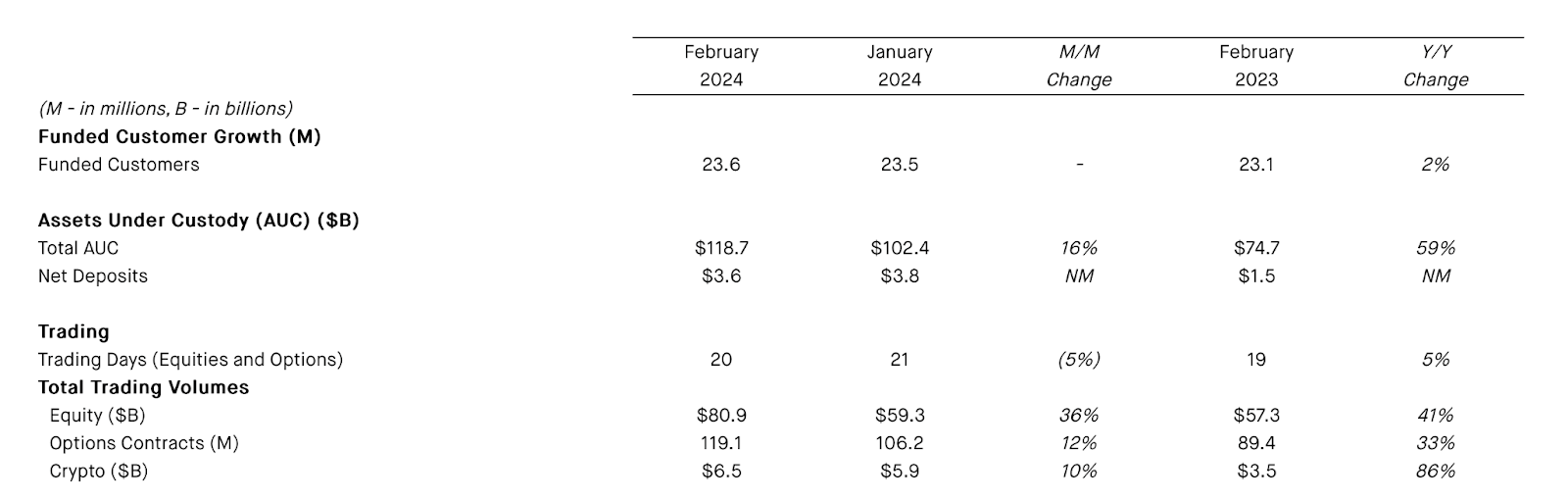

I find it likely that the company will start to see stronger growth in transaction-based revenues because it will lap easier comparables, helping to offset the slower net interest revenue growth. The company’s February operating update as well as the January operating update both showed strong growth in trading volumes. Trading volume growth has not correlated one-for-one with transaction fee growth but should provide some directional guidance on what to expect in the upcoming quarters.

February Operating Update

I note that the Robinhood Gold Card was not released until the end of March, and thus the company might see the strong growth carry forward into the second quarter (and beyond).

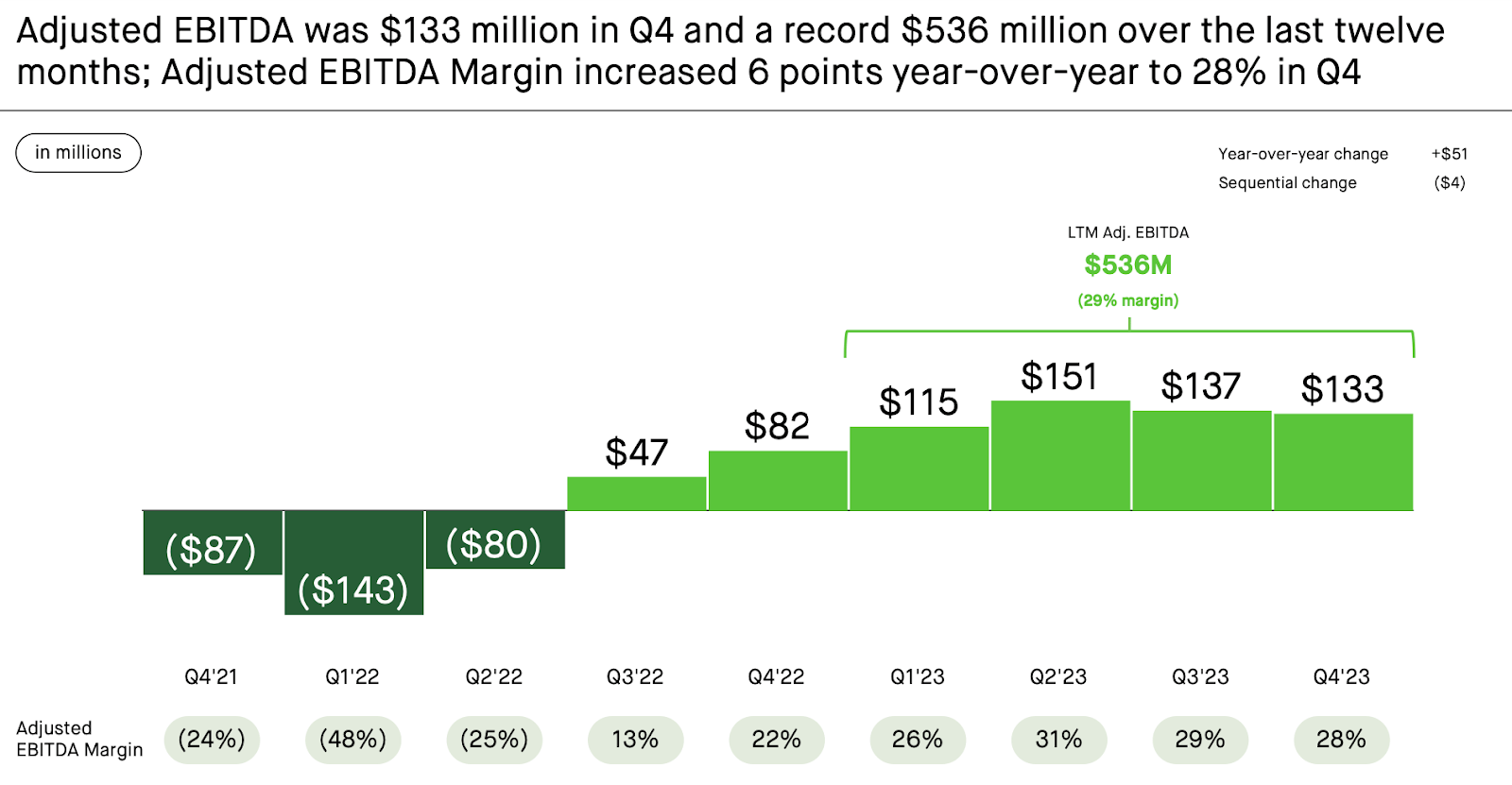

HOOD generated $133 million in adjusted EBITDA in the fourth quarter, representing 62% YoY growth and a 28% margin.

2023 Q4 Presentation

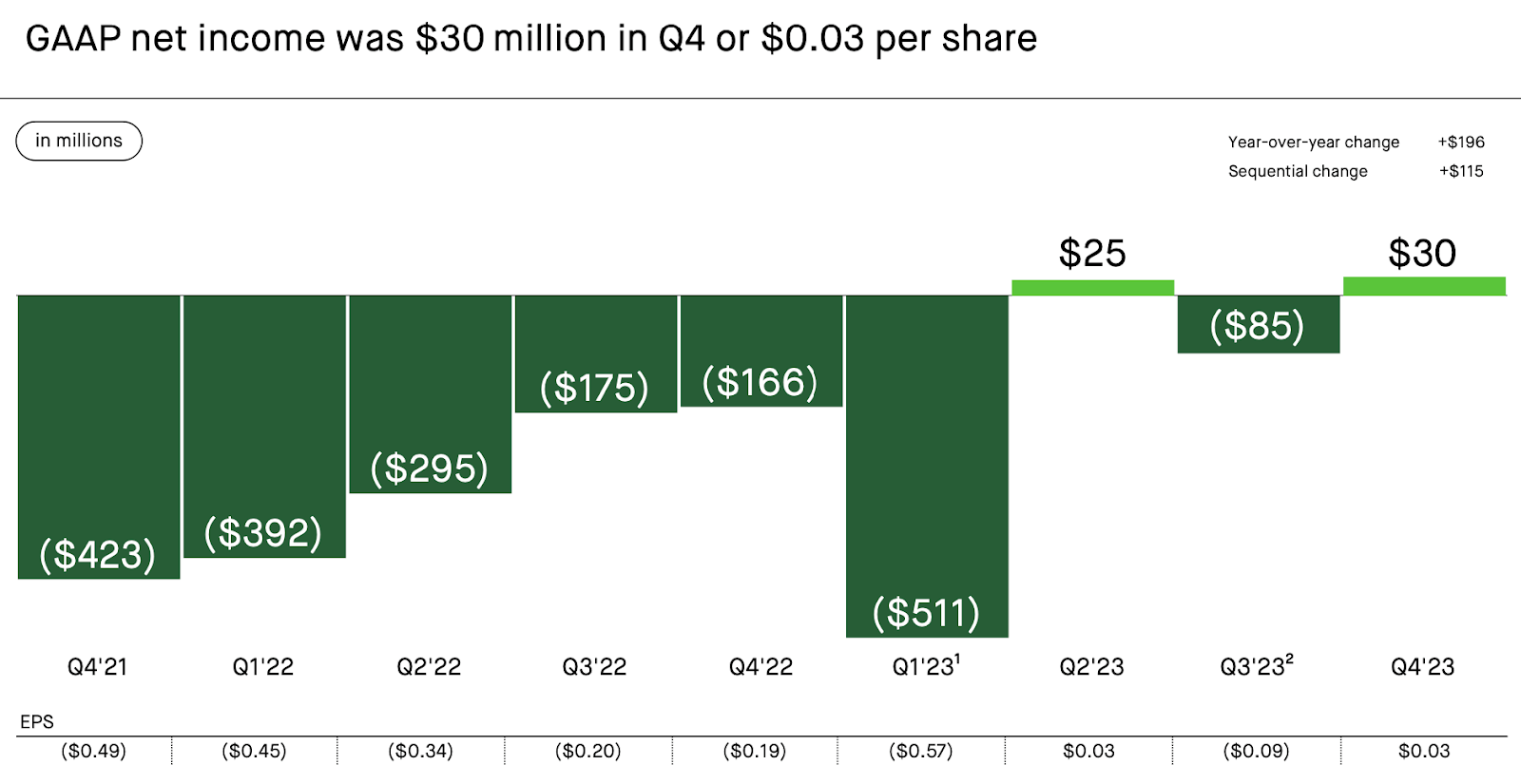

On a GAAP basis, the company generated $30 million in net income. The company showed great cost discipline following the pandemic and is benefitting from operating leverage.

2023 Q4 Presentation

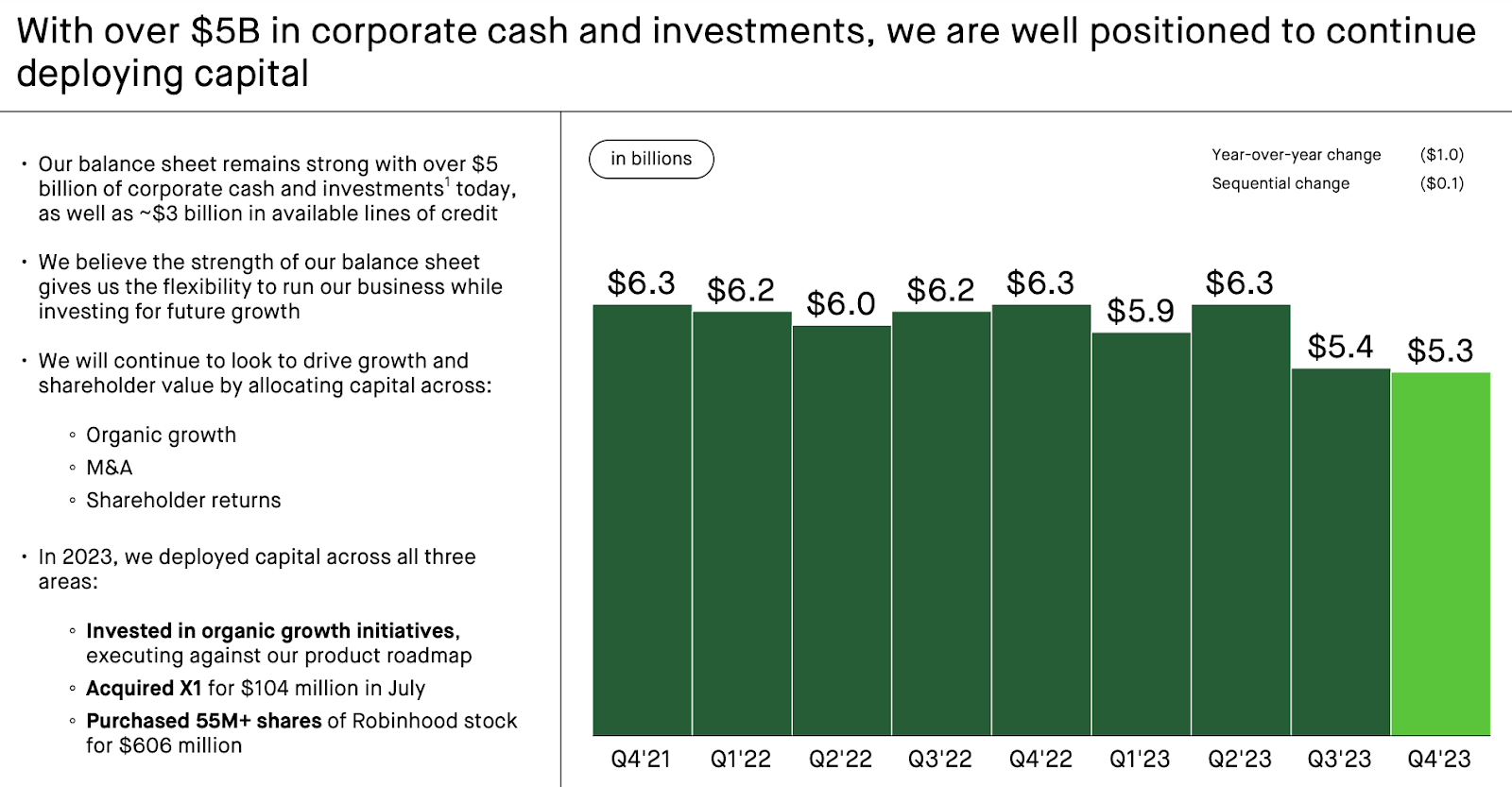

HOOD ended the quarter with $5.3 billion in corporate cash versus no corporate debt. The large cash position helps to reduce the downside risk as well as generate valuable interest income.

2023 Q4 Presentation

On the conference call, management offered one data point which should not be overlooked. Management noted that they had “$1.3 billion of net positive brokerage account transfers into Robinhood” and that they had “already exceeded that total halfway through Q1.” I again note that the company did not release their new credit card until the end of March. Management had not discussed account transfers for all of 2023 – account transfers refer to transferring assets from one brokerage firm to another. I suspect that HOOD had seen net negative brokerage account transfers for many quarters due to its reputational hit amidst the meme-stock fiasco. With MAU growth stabilizing, transaction-based revenue growth returning, and now brokerage account transfers turning positive, it appears that HOOD has finally moved beyond GameStop (and any drama from the other memes).

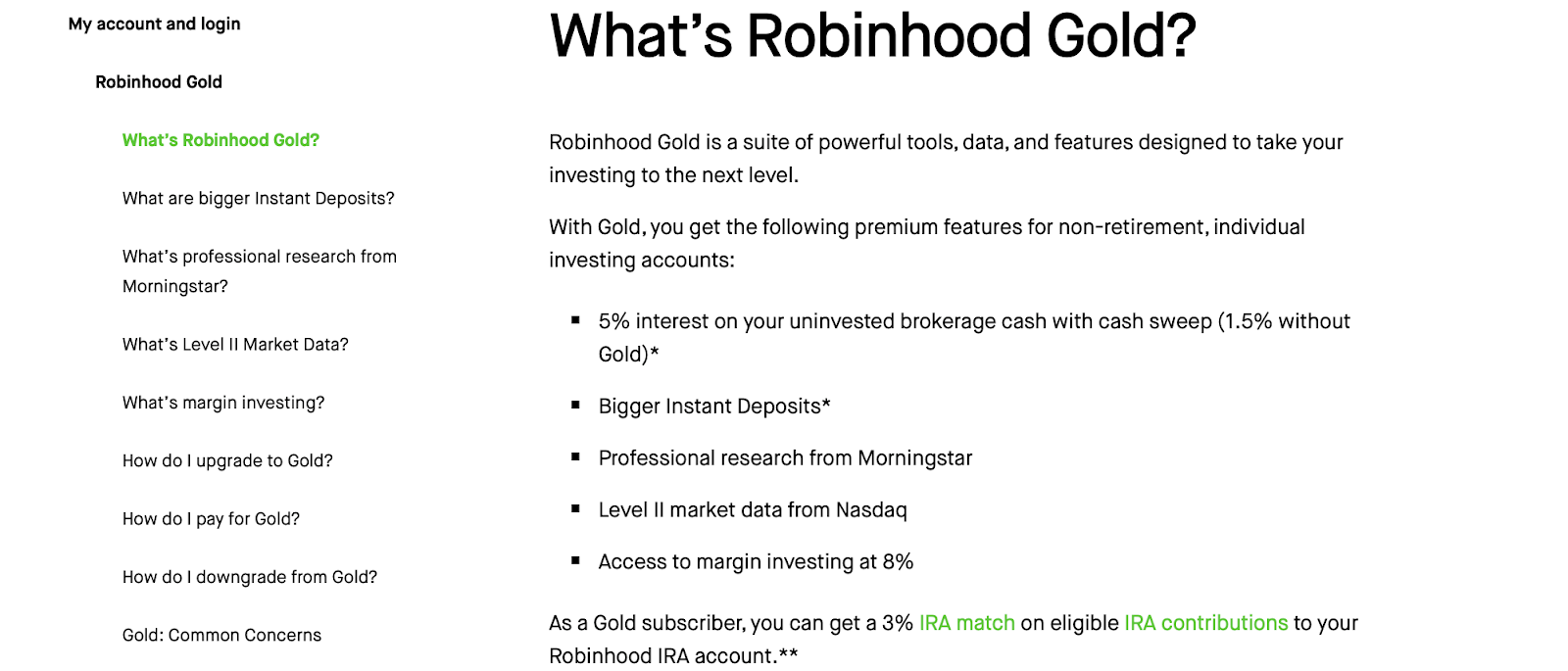

Management also noted that Gold subscriber growth stood at 25% YoY to 1.42 million, which is significant due to Gold subscribers representing a more lucrative customer base. Management noted that Gold ARPU were “multiples” of the average customer, had:

“more than eight times the assets with an average of about $40,000, grew net deposits more than twice as fast, and have adopted our products at higher rates.”

As a reminder, HOOD offers Gold subscribers various perks such as 5% interest on uninvested brokerage cash and lower margin interest rates.

Robinhood

Management discussed the Gold subscriber perks as being something that competing brokerage firms typically offer only to “their high net worth customers,” and explicitly noted their expectation for their Gold product to “disrupt the wealth management industry just in the same way that we’ve been disrupting trading.” It is curious to see HOOD manage to win market share through easily replicable practices such as promotional activity, but one should not underestimate the apparent addiction that legacy firms have on high margins and customer fees.

Is HOOD Stock A Buy, Sell, or Hold?

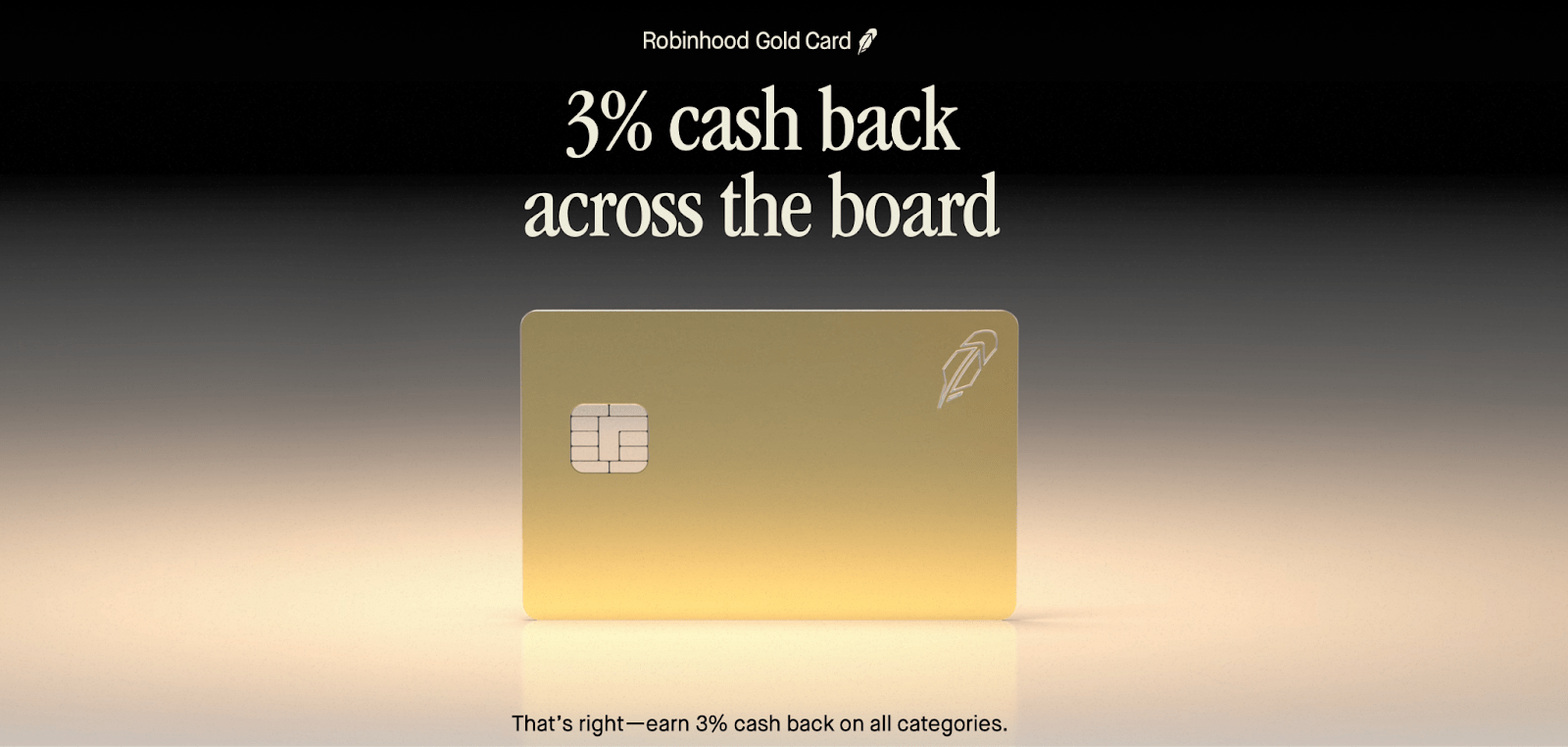

The Robinhood Gold Card looks impressive, and that’s coming from a credit card addict. The card is made of stainless steel (some members will even get cards made with actual gold) and offers 3% cash back on all purchases, among other perks.

Robinhood

As a millennial myself, I can attest that these credit card reward rates, even if they are offering low single digit returns on purchases, can build real customer loyalty. This 3% general cash back offering is the highest of any card in the market today, and I find it likely that HOOD will be able to earn many new customers because of it. Competing firms can level the playing field by boosting their own rewards rates, but as mentioned earlier, legacy firms for whatever reason seem reluctant to yield on margins even if the risk is market share loss.

Consensus estimates call for 19% YoY revenue growth this year, followed by a steep deceleration to the mid-single-digit level thereafter.

Seeking Alpha

I find this outlook to look rather conservative, especially if HOOD can build on its momentum and continue adding Gold subscribers. With the stock trading at 7x sales, the stock looks attractively valued, especially given that competing firm Charles Schwab (SCHW) trades at 6.5x sales itself. I can see HOOD sustaining at least double-digit top-line growth for many years, which could justify an 8x to 10x sales multiple (equating to a 24x to 33x earnings multiple based on my long-term 33% net margin assumption), implying solid upside between ongoing growth and multiple expansion potential.

What are the key risks? HOOD might not see growth materialize as expected. Perhaps HOOD’s promotional efforts are not enough to win over high-net-worth clients. It is also possible that competitors increase their promotional activity as well, which might eat into growth rates as well as margins. If the latter were to occur, then HOOD stock might trade at a lower earnings multiple due to the increasing price competitive nature of the business.

The key, in my view, would be winning as many customers as they could until the competition responds, and retaining these customers thereafter. It is possible that HOOD’s customer base is of a riskier profile, and thus HOOD might be exposed to greater downside risk in times of market volatility (though the company performed strongly amidst the 2022 tech stock crash).

Conclusion

I am seeing a sentiment shift in HOOD stock, driven by a potential acceleration in asset and revenue growth. The company appears to be back to taking market share, and I am optimistic that the Robinhood Gold Card can help build momentum in this respect. The company’s cash hoard remains an important asset, and the stock looks reasonably valued in light of the ongoing momentum. I reiterate my Buy rating for the stock.

Read More:Robinhood: Disrupting Industry Incumbents With Gold-Plated Cards (NASDAQ:HOOD)

2024-04-16 15:02:47