(Kitco News) – Gold remains under-allocated in investor portfolios, and the Fed’s imminent easing cycle will likely make it an even more attractive asset this year, according to Columbia Business School professor and QuantStreet Capital partner Harry Mamaysky.

In an in-depth analysis of gold’s investment prospects published by Advisor Perspectives, Mamaysky begins by addressing the performance of the hottest current alternative asset, Bitcoin, which “has skyrocketed in the weeks after the introduction of bitcoin ETFs.”

“The above chart shows the spot price of bitcoin over the last three years, along with its hockey stick appreciation thus far in 2024,” he wrote. “Alongside bitcoin is plotted the price of gold (the front gold futures contract from COMEX). The bottom chart shows their ratio, i.e., the price of a troy ounce of gold in units of bitcoin.”

“Gold prices, denominated in units of bitcoin, have plunged close to their all-time lows from late 2021,” he noted.

However, Mamaysky said that many of the arguments that favor investment in bitcoin also apply to gold. “Gold is a store of value that has been a good inflation hedge in the long run,” he said. “Gold is in limited supply (barring major advances in space exploration). Gold is easy to trade because there are multiple liquid ETFs that allow investors to allocate to it in their brokerage accounts. And should the internet ever go dark (hopefully this will never happen), gold will still sit safely in its vaults, whereas bitcoin… well, you know.”

He added that his goal “is not to philosophize about gold versus bitcoin as non-dollar stores of value, but that the likely start of a Fed easing cycle later in 2024 may serve as a catalyst for the price of gold.”

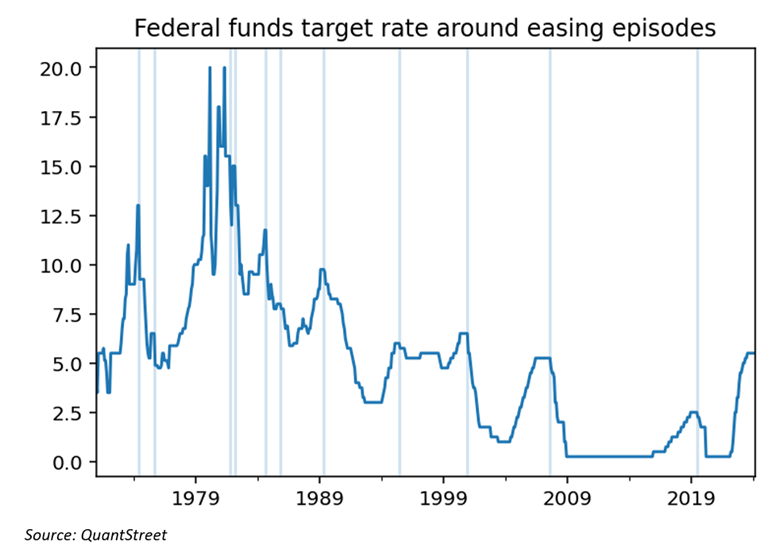

Mamaysky then looked at the Fed funds target rate over the last 50 years. “The vertical blue lines identify periods of Fed easing, defined as a drop in the Fed funds rate after it had been unchanged for two meetings with a peak fall of over 1.5%,” he said.

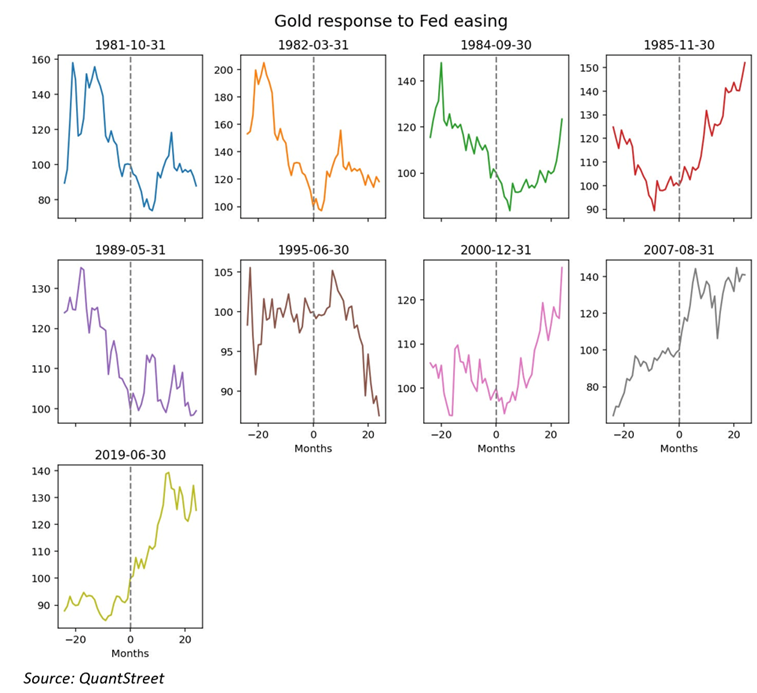

He pointed out that according to this definition, there have been 11 periods of Fed easing since the 1970s, with the most recent kicking off in December 2000, August 2007, and June 2019. He then looks at “the behavior of gold futures prices in the two-year period prior to and after the start of each easing episode.”

“Outside of the very minor easing episode that started in 1995, gold futures were either flat or up in the subsequent two years in all cases,” Mamaysky noted. “Aggregating the performance of gold futures, normalized to start at 100 at the end of the easing month, across all nine episodes, on average, gold futures prices increased by just under 20% in the two-year period after the start of Fed easing.”

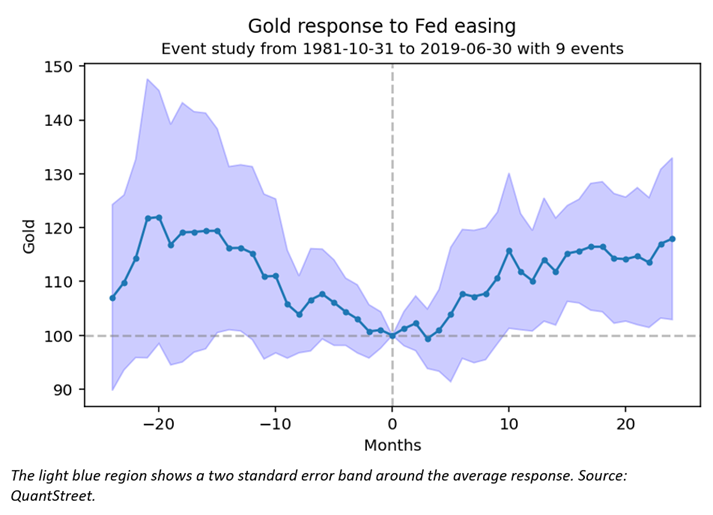

The dark blue line shows the average response, and the lighter blue region around the dark blue line shows the precision with which the average response is estimated,” he added. “Most of the responses happened in the year after the start of Fed easing.”

“As of the time of this writing, Fed funds futures are forecasting a start to the Fed easing cycle around July of 2024,” he said. “Should history repeat itself – never a guarantee – gold may do quite well over the subsequent year or two.”

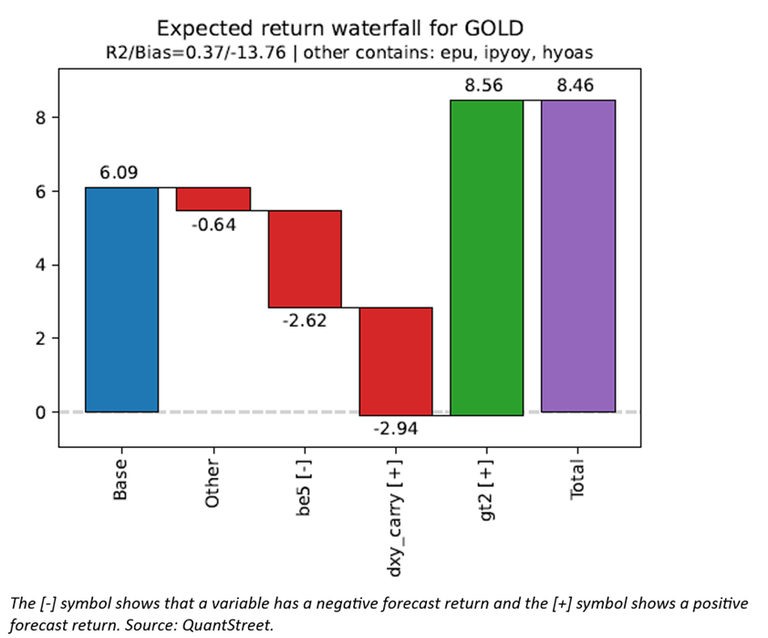

Mamaysky acknowledged that the historical analysis may not be enough to “make buying gold a compelling trade,” so he also shares corroborating evidence based on “QuantStreet’s machine learning-based forecasting model for year-ahead gold price appreciation.”

“The blue bar at the left shows the average gold return in the model training window,” he wrote. “This is the one-year ahead return – called the unconditional forecast – the model would predict if all forecasting variables were equal to their average values in the training window.”

“The red and green bars show the adjustment to the unconditional forecast because forecasting variables are either above or below their average values in the training window,” he explained. “The be5 variable shows that the currently high level of the 5-year breakeven spread (the difference in yields between nominal Treasury securities and TIPS) forecasts gold returns negatively. I interpret this to mean that when inflation expectations are elevated (and they are slightly elevated today) investors buy gold as a hedge, which drives up gold prices, dropping gold’s expected returns.”

“The dxy_carry variable, which measures the yield differential between 10-year Treasury bonds and bunds, forecasts gold returns positively,” he noted. “My interpretation is that when U.S. rates are high relative to international rates, it becomes costly for international investors to own gold instead of owning the high-yielding dollar. This drives down the price of gold, thus driving up its expected returns.”

Mamaysky pointed out that current U.S. rates “are closer to bund rates than they were in the model estimation window,” which serves to lower gold’s forecasted return.

“Finally, gt2 shows that when U.S. 2-year rates are higher than their average value during the training window, as is now the case, next one-year gold returns are on average high,” he said. “The reason is that, with high domestic rates, U.S. investors may find it costly to hold gold, a zero-yielding asset, thus lowering the demand curve for gold, driving down its price, and driving its expected returns higher.”

Mamaysky said the net effect of these adjustments raises the unconditional one-year ahead gold return forecast to a rate of 8.46%.

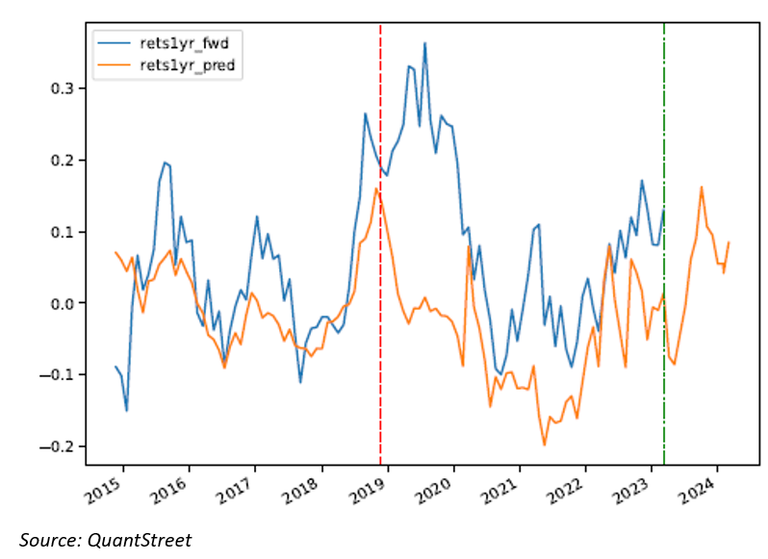

“How accurate has the model forecast been historically? The next figure shows the model’s out-of-sample one-year ahead return forecast (the orange line) lined up with the actual year-ahead gold return (the blue line),” he said. “QuantStreet’s forecasting model has generally worked well in this out-of-sample forecasting exercise.”

Mamaysky said that when the adjusted machine learning forecast is combined with “gold’s positive trend over the past year (up over 14%)” the yellow metal’s prospective returns are attractive, especially when considering gold’s low correlation with most risk assets.

“QuantStreet’s asset allocation framework is currently calling for a gold exposure across all risk-targeted portfolios,” he said. “The potential catalyst of an impending Fed easing cycle is icing on the cake.”

Mamaysky noted that “the current gold to CPI ratios is extremely high” in historical terms, and that the recent run-up in the gold price “appears to coincide (somewhat) with the introduction of the GLD ETF in November 2004, which made gold investing easily accessible to retail investors.”

“Arguably, the presence of a liquid gold ETF has moved gold valuation permanently into a different regime,” he said, adding that the underlying study suggests that “gold is an under-owned asset class and perhaps the presence of liquid gold ETFs chipped away at this problem.”

“The negative is that the gold price relative to the CPI index already reflects some of these considerations,” Mamaysky concluded. “Nevertheless, there is enough to warrant a tactical allocation to gold in investor portfolios.”

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Kitco Metals Inc. The author has made every effort to ensure accuracy of information provided; however, neither Kitco Metals Inc. nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in commodities, securities or other financial instruments. Kitco Metals Inc. and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.

Read More:Gold’s year-ahead returns projected at 8.46%, Fed cuts are ‘icing on the cake’ – QuantStreet Capital’s Mamaysky

2024-03-19 16:53:17