Sean Anthony Eddy

Since Michael Murray took the helm as CEO at Kopin Corp. (NASDAQ:KOPN) last year, the company’s operational efficiency has seen a boost, thanks to his visionary leadership and dedication to the company’s restructuring, which included an announced overhaul of the company’s OLED production unit. Michael Murray’s focus on strong customer relationships and timely product delivery is making a real impact, leading to an increase in orders from customers.

Kopin has been in the business of providing components and solutions for wearable products for military, enterprise, industrial, medical, and consumer markets since 1990. The company’s product line includes AMLCD, FLCOS, OLED, and Micro LED displays, as well as optical modules and low-power ASICs. Kopin’s current focus is the development of innovative display technologies, like the NeuralDisplay, and proprietary AI-powered firmware and software solutions for augmented and virtual reality (AR/VR) wearables. NeuralDisplay is a significant advancement in AR/VR. NeuralDisplay is designed to incorporate sensors (using advanced sensor fusion) that can detect and respond to a user’s environment and physiological responses in real time. By utilizing AI, NeuralDisplay can dynamically adjust display settings, such as brightness and contrast, to suit users’ immediate needs and reactions, potentially reducing common discomforts associated with AR/VR usage, like eye strain and motion sickness.

The incorporation of “neural” capabilities into AR/VR displays aligns with Kopin’s strategic vision of creating advanced human-centric display solutions. NeuralDisplay’s ability to adapt to the user rather than the other way around is a key differentiator that could address some of the barriers to widespread AR adoption. By focusing on such user-adaptive technologies, Kopin is positioning itself to meet the evolving demands of both the defense and consumer markets, where the need for advanced AR/VR solutions is growing and the market size is expanding.

VR in Aerospace and Defense Market Size (Fortune Business Insight)

Immersive technologies like AR/VR are gaining popularity in the aerospace and defense sectors. The growing demand for AR/VR in this sector is mainly driven by the adoption of simulation training for military personnel, as this provides a lower operational cost compared to conventional training environments, among other advantages. The global VR in Aerospace and Defense market size is expected to reach $5.84 billion by 2026, exhibiting a 37.9% CAGR between 2015 and 2026. The North America VR in aerospace and defense market size was $136.3 million in 2018.

Kopin has secured significant military contracts that underscore the growing integration of AR/VR technologies in defense applications. In August, the company announced a $12.8 million follow-on order from a Department of Defense prime contractor for its AR module called eyepiece subassembly. This is in addition to a separate $1.9 million follow-on order for a Non-Recurring Engineering (NRE) thermal weapon sight program.

In September, Kopin received an additional $3.4 million follow-on order for its high-brightness liquid crystal displays for the F-35 Joint Strike Fighter program, with production expected to continue through 2030. Kopin has been the go-to supplier for microdisplays in the F-35 pilot helmets since inception.

Kopin also has an ongoing collaboration with General Dynamics (GD) combat systems segment for display systems for an armored vehicle upgrade program. Kopin could generate revenue of up to $100 million over the lifetime of the program.

These follow-on orders, alongside ongoing collaborations with GD, show Kopin’s pivotal contributions to the advancement of AR/VR applications within the military domain, with the potential to revolutionize training, operations, and equipment for defense personnel, and gain significant market share in the process.

A Look at Q3 Numbers

Kopin released its Q3 2023 earnings result last month, beating the consensus EPS estimate by $0.02 and revenue by $565.83k.

Q3 2023 Income Statement (Company 10-Q)

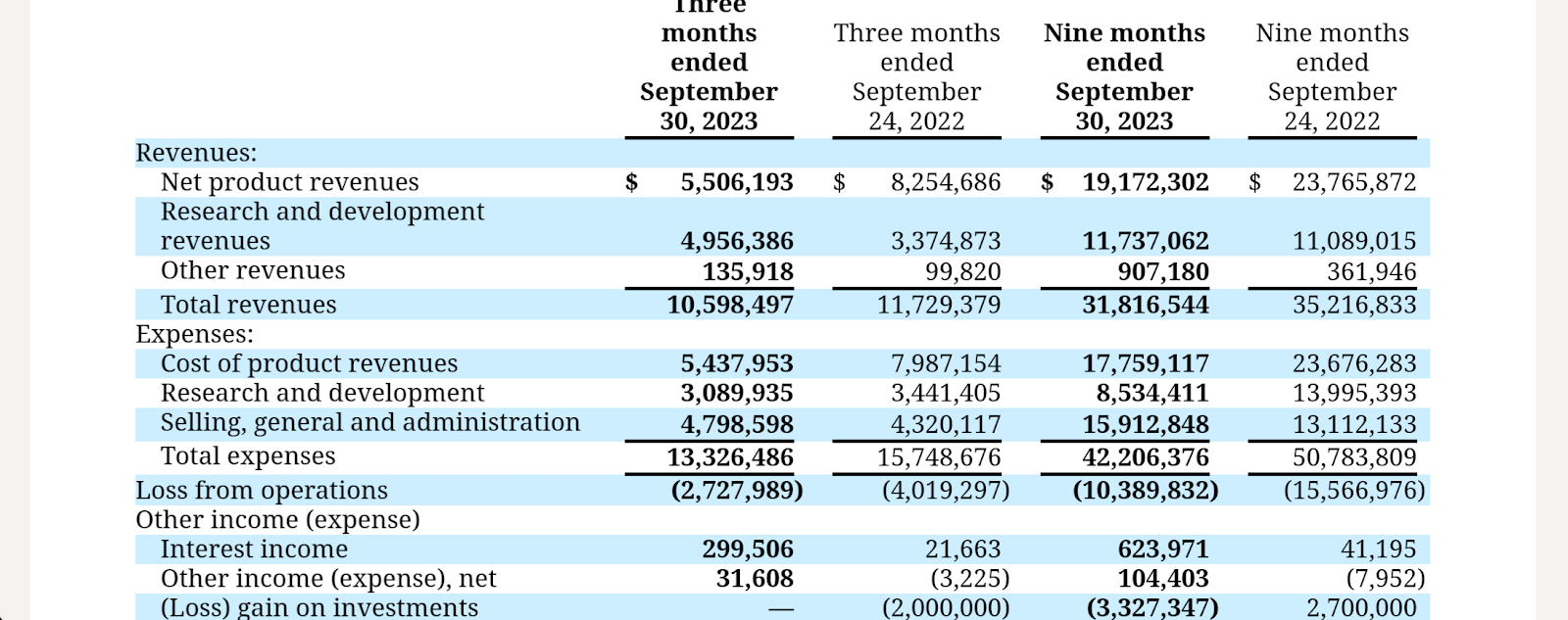

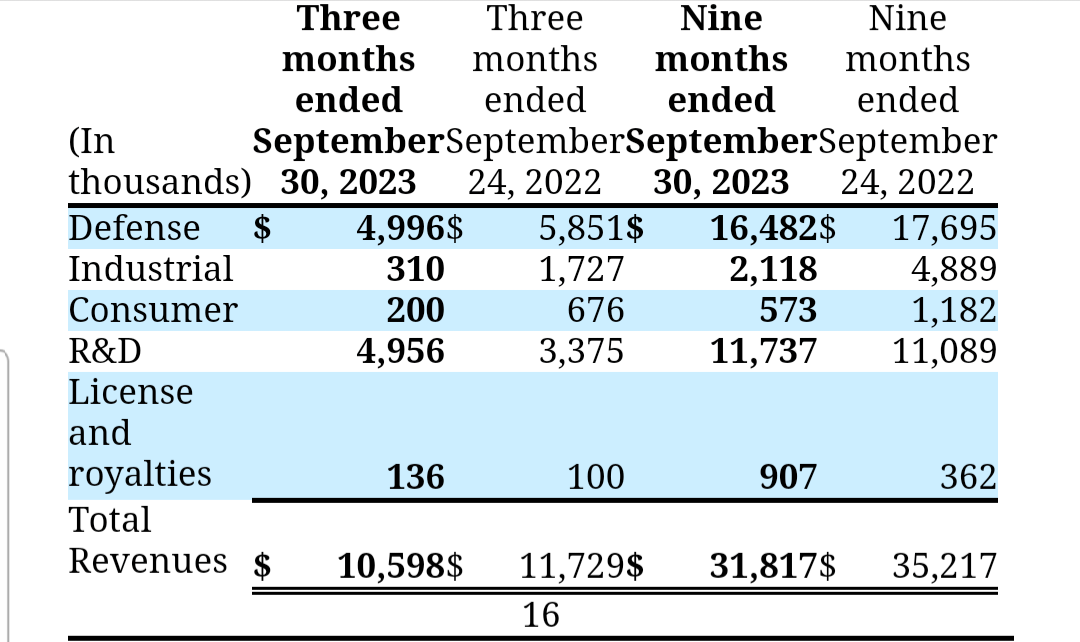

Kopin Corporation’s third-quarter financials show a mixed bag of results. The company’s total revenues for Q3 2023 stood at $10.6 million, which represents a 10% YoY decrease from the $11.7 million total revenue reported in Q3 2022.

Disaggregated Revenue (Company 10-Q)

Industrial revenues saw a $1.4 million YoY decline due to weakness in the 3D automated test market in China; this impacted the total revenue. Defense revenues also saw a contraction, decreasing by $800k or 14% YoY. The decline was caused by changes in the pattern of the purchase orders made by customers in the defense sector.

However, it wasn’t all a downward trend in disaggregated revenue for Q3. Research and Development revenues jumped 47% to $5.1 million. The surge is related to the R&D big lump NRE order of $1.9 million received for a thermal weapon sight program mentioned earlier. This R&D revenue surge underscores Kopin’s robust innovation pipeline and the value placed on its R&D capabilities by the market, particularly in the defense sector.

COGS remained relatively flat YoY at ~99% of product revenues, indicating a stable production cost structure amidst fluctuating sales. R&D expenses saw a 10% YoY decrease to $3.1 million, reflecting the company’s strategic efforts to rationalize operations and focus on high-potential projects. SG&A expenses rose to $4.8 million for the quarter, driven by an increase in legal expenses and non-cash stock compensation expenses, which were partially offset by a decrease in compensation and benefit costs.

Despite the lower revenues, Kopin’s saw an improved bottom line. Net loss shrank to about $2.5 million or -$0.02 per share, compared to a net loss of $6.1 million or -$0.07 per share in Q3 2022. This improvement in net loss is indicative of Kopin’s concerted efforts to streamline operations and control costs, even as they navigate a dynamic market landscape with ever-changing demands and customer needs.

Kopin’s improved financial health is further evidenced by an increase in its cash and marketable securities to about $21.7 million at the end of Q3, compared to a value of $12.6 million at the end of 2022. Since the start of the current fiscal year, Kopin’s cash and marketable securities have increased by about 72%. The current value at the end of Q3 represents a ~44% YoY increase.

Kopin’s Growth Momentum

Kopin’s Q3 earnings call brought to light a key metric that signals the company’s forward momentum: the book-to-bill ratio. The book-to-bill ratio is a measure that compares the amount of orders received (bookings) to the amount of products shipped and billed (billings).

In Q3 2023, Kopin reported a robust book-to-bill ratio of approximately 2:1. This means Kopin received two times the amount of new orders compared to the revenue generated during the quarter. For every $1 in revenue, Kopin received $2 in new orders. This impressive figure is a testament to the company’s strong order intake and also suggests a current uptick in demand for Kopin’s products. The fact that this is the fourth consecutive quarter where Kopin has achieved a positive book-to-bill ratio adds to the narrative of sustained demand and provides a glimpse into the company’s potential for revenue growth and stability.

The consecutive positive book-to-bill ratio bodes well for Kopin’s future revenue growth. It reflects the company’s ability to attract new business and retain existing customers in a competitive market. It also points to a healthy order backlog, which can lead to more predictable and potentially increasing revenue streams. With this momentum in consecutive new orders and revenue growth potential, coupled with the improved operating margin trend, I believe, Kopin is tending towards profitability.

Valuation

The current P/S ratio of 3.46x is slightly higher than the sector median P/S of 3.00x and lower than Kopin’s 5-year historical P/S of 5.18x, suggesting that the stock is trading at a discount relative to its sales historical valuation. With lower long-term debt on its balance sheet compared to its long-term assets, investors looking for a company with lower financial risk could consider this a positive sign.

The EV/Sales ratio of 2.95x, which is 31% lower than its historical 5-year average EV/Sales of 4.76x, indicates that the market is currently valuing Kopin’s revenue stream at a significant discount to the historical average. This could suggest that the stock is undervalued based on this metric, potentially offering a more attractive entry point for investors.

Takeaway

The new CEO’s emphasis on customer retention and timely product delivery is great, and I think it is working well for the company. This is already shown in the number of follow-on orders the company has received this fiscal year, and in its positive book-to-bill ratio over several quarters. This customer-centric strategy is particularly prudent given the inherent difficulties associated with securing new clients in some of the sectors (aviation and defense) that Kopin serves, where barriers to entry are high and the emphasis on reliability and trust is paramount.

As the company continues to execute on these fronts, investors need to monitor how these efforts translate into financial performance and market share expansion.

Read More:Kopin Stock: Visionary Leadership Fuels Growth And Market Potential (NASDAQ:KOPN)

2023-12-16 03:45:41