An important thing to keep our eyes on these days.

By Wolf Richter for WOLF STREET.

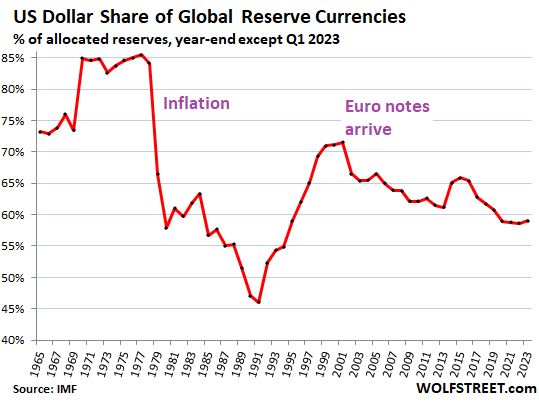

The US dollar as dominant global reserve currency has been on a slow long-term downward trend, interrupted by upticks. And now we had an uptick, when the dollar gained share.

The share of the USD as global reserve currency rose to 59.0% in the first quarter of 2023, after having dropped to 58.6% in Q4, which had been the dollar’s lowest share since 1994, according to the IMF’s recent COFER data.

The US dollar as global reserve currency means that foreign central banks and foreign official institutions hold USD-denominated assets, such as Treasury securities, agency securities, corporate bonds, mortgage-backed securities, etc. They also hold competing foreign exchange reserves in other currencies, such as in euros (#2), and in yen (#3). But holdings in their own local currency are not foreign exchange reserves and are not included; so the Fed’s holdings of US Treasuries and MBS are not included; the ECB’s euro-denominated assets are not included, etc.

What happened in 1978 that caused the dollar’s share to collapse from 85% to 46% by 1991? After inflation exploded in the US in the late 1970s, the world lost trust in the Fed’s ability to manage inflation. Even as inflation backed off in the 1980s, it took a long time for the world to regain confidence in the dollar. When it did, the dollar’s share rebounded until the euro came along and stopped that bounce in its tracks. Since then, the euro has been the undisputed #2 global reserve currency with a share of around 20%.

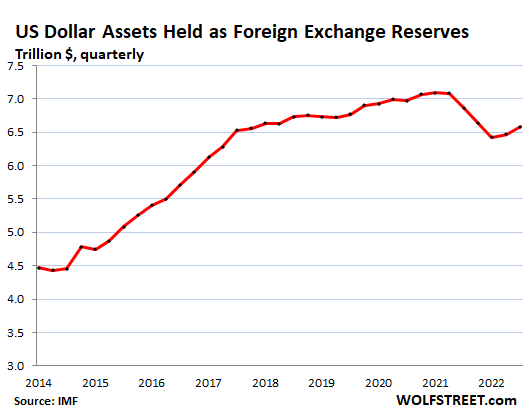

In dollar terms, the holdings of USD-denominated assets at central banks other than the Fed rose to $6.58 trillion, the second quarter in a row of increases, after three quarters in a row of declines.

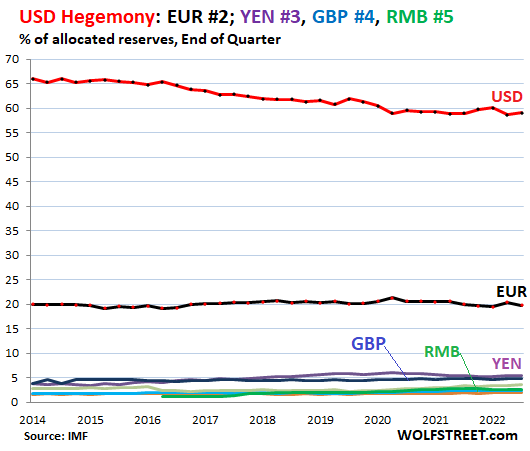

The other major reserve currencies.

The euro, perennially #2: Its share dipped in Q1 to 19.8%, from 20.4% in the prior quarter. The old dream of “parity” with the dollar as reserve currency has not yet come true. And at the current rate, it’s going to take a very long time and will require lots of patience.

The Japanese yen, #3: Share of 5.5%, unchanged (purple in the chart below).

The British pound, #4: Share of 4.9%, unchanged (blue, just under the yen).

The Chinese renminbi, #5: its share has now dipped for four quarters in a row to 2.58%, the lowest since Q1 2021 (thick green line). The progress that had been expected has been waylaid by the reality of capital controls, convertibility issues, and other issues. Central banks appear to be leery of holding RMB-denominated assets. At this pace and direction, the RMB will never get close to the USD as reserve currency. China, as the second largest economy in the world, should have a larger share of global reserve currencies, but it’s just not happening.

The other currencies in the pile at the bottom: Canadian dollar (2.43%, up a hair), Australian dollar (1.98%, up a hair), and Swiss franc (0.25%, up a hair). The other currencies, each with a share even smaller than the Swiss franc’s share, have a combined have a share of 3.65%.

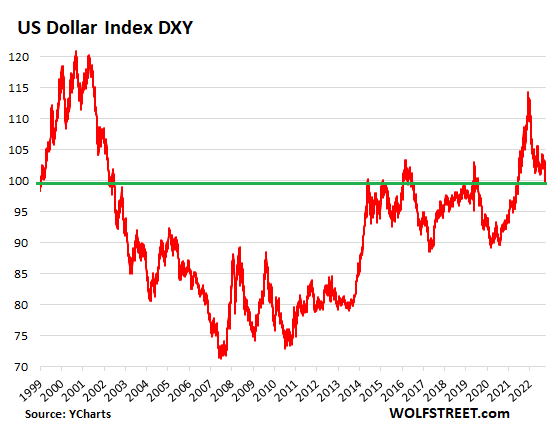

Dollar-exchange rates and foreign exchange reserves.

Foreign exchange reserves are measured in dollars. So for reporting and comparison purposes, the holdings in EUR, YEN, GBP, RMB, etc. are translated into USD figures at the exchange rate at the time. And so the exchange rate between the USD and other reserve currencies impacts the magnitude of the non-USD assets – but not of the USD-assets.

For example, Japan holds EUR-denominated assets. The value of these foreign exchange reserves is translated into USD at the EUR-USD exchange rate at the time. So the magnitude of Japan’s holdings of EUR-assets, when it’s expressed in USD, fluctuates with USD-EUR exchange rate, even if Japan’s holdings don’t change.

On a quarterly basis, the share of these holdings can fluctuate based on the exchange rate between the USD and other currencies.

But the USD exchange rates can move wildly against other individual currencies. For example, for the past 12 months, the yen has been a big mess due to the toxic mix of surging inflation and the Bank of Japan’s stubborn refusal to back off its negative policy rates and yield curve control. We just discussed this here.

Despite these fluctuations, the USD, as tracked by the Dollar Index [DXY], which is dominated by the euro and yen, is back were it was in 1999. It worked off the huge spike that peaked late last year and is now back down at the upper end of the normal range of the past two decades. So over the longer term, there is some stability between these exchange rates, though they can swing wildly in between, and they’re doing a lot of swinging right now (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Read More:US Dollar’s Status as Global Reserve Currency on Slow Long-Term Decline, but Not Going Down in a Straight Line

2023-07-16 01:53:26